An emergency fund is a financial safety net designed to cover unexpected expenses—job loss, medical bills, car repairs, or urgent home maintenance. It’s not an investment; it’s peace of mind. But where should you keep it? Two common options are high-yield savings accounts (HYSAs) and certificates of deposit (CDs). Both offer more interest than traditional savings accounts, but they differ significantly in flexibility, access, and return potential. Choosing the wrong one could leave you scrambling when you need cash fast—or earning less than you could.

This guide breaks down the real differences between high-yield savings and CDs, evaluates their strengths and weaknesses for emergency fund use, and provides actionable advice so you can confidently decide where to park your rainy-day money.

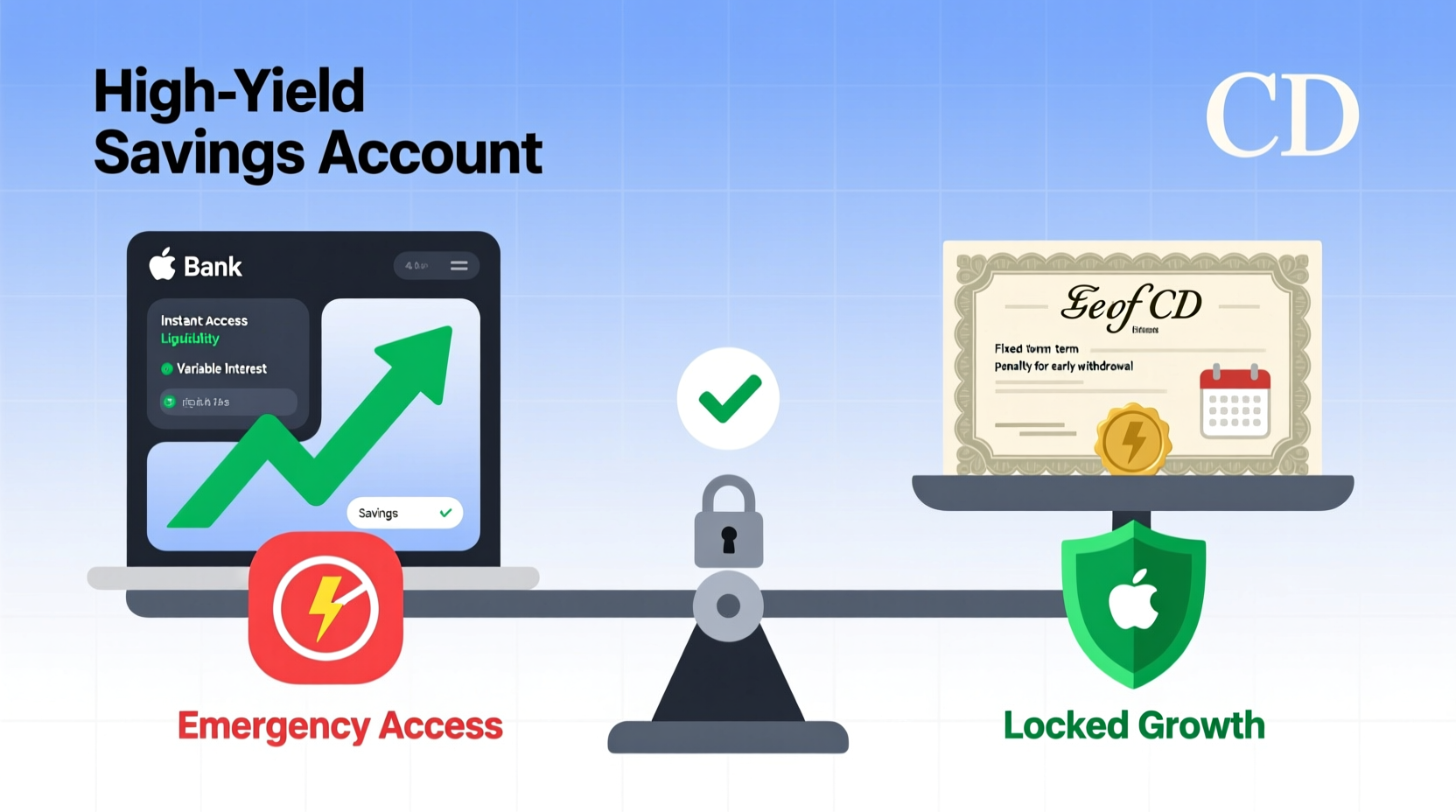

Understanding High-Yield Savings Accounts

A high-yield savings account is a type of savings account that offers a significantly higher annual percentage yield (APY) than standard bank savings accounts. These accounts are typically offered by online banks, which have lower overhead costs and pass those savings on to customers in the form of better interest rates.

HYSAs are FDIC-insured up to $250,000 per depositor, per institution, making them one of the safest places to store emergency funds. Most allow unlimited deposits and up to six withdrawals or transfers per month under federal Regulation D (though many banks now waive penalties for exceeding this limit).

The key advantages of HYSAs include:

- Liquidity: Funds are accessible within days, often instantly via linked checking accounts.

- No lock-up period: You can withdraw money at any time without penalty.

- Competitive APYs: As of 2024, top-tier HYSAs offer APYs between 4.00% and 5.50%, depending on market conditions.

- Low minimums: Many require only $1 or no minimum balance to open.

How Certificates of Deposit Work

A certificate of deposit (CD) is a time-bound savings product. When you open a CD, you agree to keep your money deposited for a fixed term—anywhere from three months to five years—in exchange for a guaranteed interest rate. Early withdrawal usually incurs a penalty, often equal to several months’ worth of interest.

Like HYSAs, CDs are FDIC-insured up to $250,000, ensuring your principal is protected. They’re ideal for savers who want to earn predictable returns without market risk. However, their rigid structure makes them less suitable for emergency funds unless carefully structured.

CDs typically offer slightly higher interest rates than HYSAs, especially for longer terms. For example, a 12-month CD might pay 5.00% APY, while a comparable HYSA pays 4.75%. But that extra 0.25% comes at the cost of accessibility.

“Liquidity is the cornerstone of an emergency fund. If you can’t access your money when disaster strikes, it’s not truly an emergency fund.” — Laura Adams, Personal Finance Expert and Author of *Money Girl's Smart Moves*

Comparing Key Factors: HYSA vs CD

To determine which option suits your emergency fund best, consider these critical factors: liquidity, returns, safety, flexibility, and ease of management.

| Factor | High-Yield Savings Account (HYSA) | Certificate of Deposit (CD) |

|---|---|---|

| Liquidity | Immediate access; funds available within 1–3 business days | Locked until maturity; early withdrawal penalties apply |

| Interest Rate | Variable APY (currently 4.00%–5.50%) | Fixed APY (often 0.25%–0.75% higher than HYSA for same term) |

| Safety | Fully FDIC-insured | Fully FDIC-insured |

| Flexibility | Deposit and withdraw freely (within federal limits) | No additional deposits; withdrawals penalized |

| Best For | Active emergency funds needing frequent access | Stable funds you won’t need soon |

When a CD Might Make Sense for Emergency Savings

At first glance, CDs seem incompatible with emergency funds due to their lack of liquidity. However, there’s a strategic approach called **CD laddering** that can blend safety, yield, and partial access.

A CD ladder divides your emergency fund across multiple CDs with staggered maturity dates. For example, if you have $12,000 in emergency savings, you might allocate:

- $3,000 into a 3-month CD

- $3,000 into a 6-month CD

- $3,000 into a 12-month CD

- $3,000 into an 18-month CD

As each CD matures, you can either reinvest it into a longer-term CD or roll it into a HYSA for immediate access. This method ensures that part of your fund becomes liquid every few months, reducing the risk of needing to break a long-term CD early.

Some banks also offer **no-penalty CDs**, which allow one penalty-free withdrawal after a short waiting period (e.g., seven days). These combine higher yields with limited flexibility, making them a hybrid option worth considering for portions of your emergency fund.

Real-Life Scenario: Choosing Between HYSA and CD

Consider Sarah, a 32-year-old marketing manager with $10,000 saved for emergencies. She lives in a city with a high cost of living and works in a competitive industry. Recently, two colleagues were laid off unexpectedly.

Sarah wants her money to grow but knows she may need quick access. She compares two options:

- Option A: A high-yield savings account offering 4.80% APY with instant transfers to her checking account.

- Option B: A 12-month CD at 5.15% APY, but with a penalty of six months’ interest if withdrawn early.

She runs a scenario: if she loses her job and needs $4,000 in month four, withdrawing from the CD would cost her about $100 in penalties and lost interest. Plus, the remaining $6,000 would still be locked. With the HYSA, she could access all $10,000 immediately, continue earning interest on the remainder, and rebuild faster.

Sarah chooses the HYSA. She values certainty and speed over a marginal gain in interest. Her decision reflects a core principle: an emergency fund must prioritize accessibility above all else.

Action Plan: How to Structure Your Emergency Fund

Here’s a step-by-step guide to help you decide whether a HYSA, CD, or combination works best for your situation.

- Determine your emergency fund target. Most experts recommend 3–6 months of essential living expenses. Calculate your monthly rent, groceries, utilities, insurance, and debt payments to set a goal.

- Assess your risk of needing quick access. Are you in a stable job? Do you have dependents? The less stable your income, the more liquidity you need.

- Compare current rates. Check reputable financial sites like Bankrate, NerdWallet, or Investopedia for the latest HYSA and CD rates. Prioritize institutions with strong customer service and mobile app functionality.

- Choose your primary vehicle. For most people, a HYSA is the default best choice. Open an account with a top-rated online bank such as Ally, Marcus by Goldman Sachs, or Capital One.

- Consider laddering CDs for excess funds. If you’ve already saved 3–6 months’ worth and want to earn slightly more on surplus cash, allocate a portion (e.g., 25%) to a CD ladder.

- Automate contributions. Set up automatic monthly transfers from checking to savings to build your fund consistently.

- Review annually. Interest rates change. Reassess your account’s APY yearly and move funds if better options emerge.

Checklist: Optimizing Your Emergency Fund Placement

- ✅ I know exactly how much I need in my emergency fund (3–6 months of expenses).

- ✅ My chosen account is FDIC-insured.

- ✅ I can access funds within 1–3 business days without penalty.

- ✅ The account earns competitive interest (at least 4.50% APY as of 2024).

- ✅ I’ve compared at least three financial institutions before deciding.

- ✅ I’ve set up automatic deposits to grow my fund steadily.

- ✅ I review my account’s rate and terms at least once per year.

Frequently Asked Questions

Can I lose money in a high-yield savings account or CD?

No, not if your account is FDIC-insured and your balance is within the $250,000 limit. Both HYSAs and CDs are among the safest places to keep emergency funds. Market fluctuations do not affect your principal.

Are CD penalties always steep?

Penalties vary by bank and term length. Short-term CDs (3–12 months) typically charge 30–90 days of interest for early withdrawal. Longer-term CDs may charge up to a full year’s interest. Always read the fee schedule before opening a CD.

Should I split my emergency fund between a HYSA and CD?

You can—but only if you structure it wisely. For example, keep 75% in a HYSA for immediate access and put 25% in a short-term or no-penalty CD to earn slightly more interest. Avoid locking all your emergency money in CDs.

Final Recommendation: Why High-Yield Savings Wins for Most People

While CDs offer marginally higher interest, the trade-off in liquidity makes them a poor fit for the core of your emergency fund. An emergency, by definition, is unpredictable. You can’t forecast when you’ll need the money—or how much.

A high-yield savings account strikes the ideal balance: strong safety, competitive returns, and instant access. It allows you to respond quickly to life’s surprises without financial penalties or stress. In rare cases—such as when you have a fully funded emergency stash and want to optimize yield on a portion—a CD ladder or no-penalty CD can complement your strategy. But for the vast majority of savers, the HYSA is the smarter, safer, and more practical choice.

“The best emergency fund feels invisible until you need it—and then it feels like a lifeline. That only happens when it’s safe, accessible, and ready.” — Jean Chatzky, Financial Editor, NBC Nightly News

Take Action Today

Your emergency fund isn’t just about saving money—it’s about building resilience. Open a high-yield savings account today, transfer your emergency fund, and automate your contributions. Even if you start small, consistency and smart placement will compound over time. Don’t let the pursuit of slightly higher returns compromise your ability to handle life’s curveballs. Protect your peace of mind first. The interest will follow.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?