Tax season often brings surprises—some welcome, others less so. If you're facing a tax bill this year, you're not alone. Millions of taxpayers end up owing money to the IRS, even when they’ve been diligent about their finances. The good news is that most of these situations are preventable. Understanding why you owe—and taking proactive steps—can help you avoid a similar outcome next year.

Owing taxes doesn’t necessarily mean you made a mistake. It may simply reflect changes in income, life events, or insufficient tax withholding. But repeated tax liabilities can strain your budget and reduce financial flexibility. By identifying the root causes and adjusting your approach, you can align your tax payments with your actual liability and potentially turn that balance due into a refund—or at least break even.

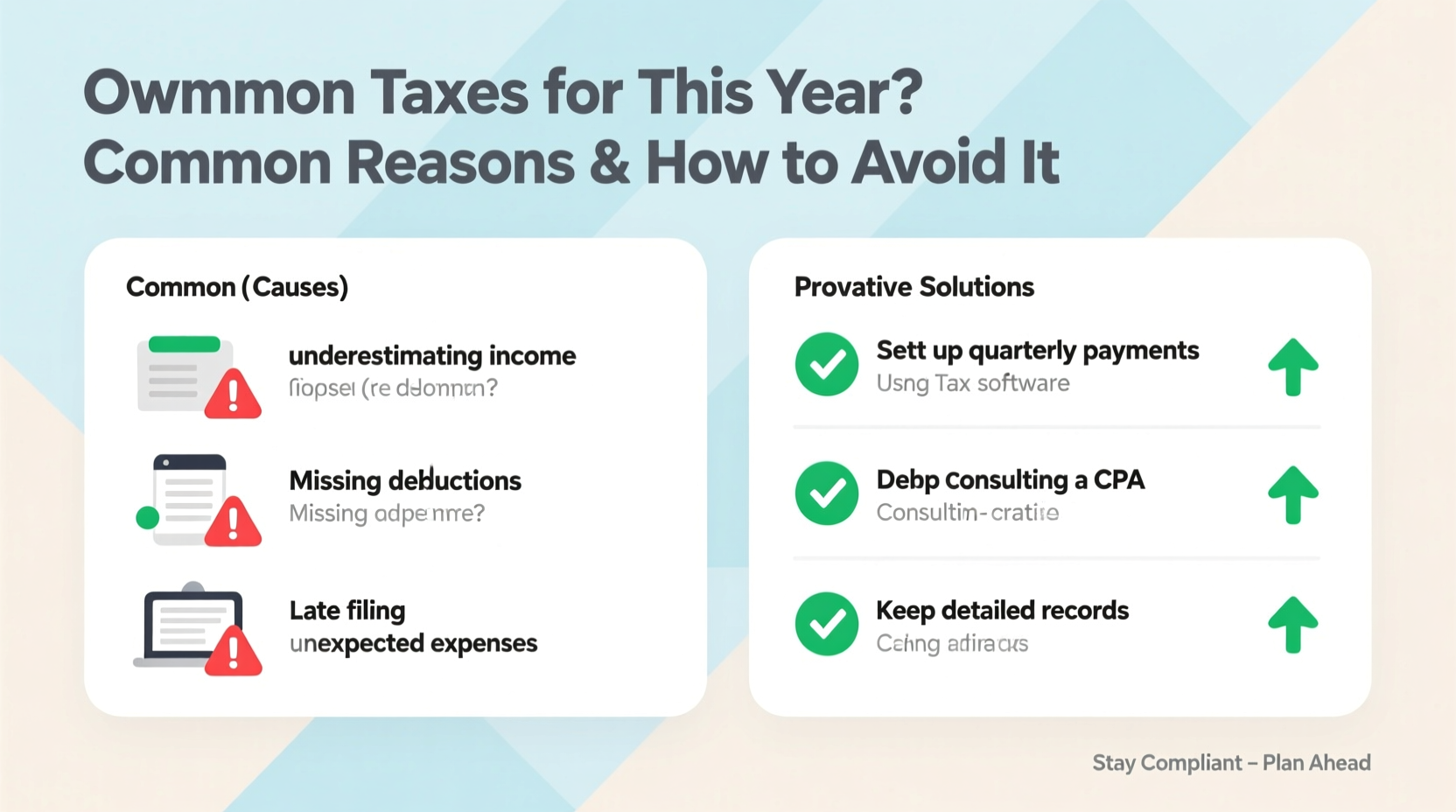

Why You Might Owe Taxes This Year

The most common reason people owe taxes is under-withholding. When you work as an employee, your employer withholds federal income tax from each paycheck based on the information you provided on Form W-4. If you claimed too many allowances or failed to update your form after a major life change, not enough tax may have been taken out during the year.

Self-employed individuals face a different challenge: no automatic withholding. Without quarterly estimated tax payments, freelancers, gig workers, and independent contractors often accumulate a large tax bill by April. According to the IRS, more than 60% of self-employed filers who don’t make estimated payments end up owing money.

Other common triggers include:

- A sudden increase in income (e.g., bonus, side hustle, investment gains)

- Failing to adjust for marriage, divorce, or a new job

- Not accounting for taxable retirement distributions

- Receiving non-wage income without withholding (like rental income or cryptocurrency gains)

“Many taxpayers are shocked by their tax bill because they didn’t realize their additional income was taxable or that they were responsible for paying taxes throughout the year.” — Lisa Reynolds, CPA and Tax Educator

How Withholding Affects Your Tax Outcome

Your paycheck isn’t just about gross vs. net—it’s also a tool for managing your annual tax obligation. The amount withheld determines whether you prepay your tax liability gradually or face a lump sum later. Think of it as forced savings for your tax bill.

If too little is withheld, you effectively receive interest-free loans from the government—but you pay them back with penalties if you fall short by too much. The IRS requires you to pay at least 90% of your current-year tax or 100% of the prior year’s tax (110% if your AGI exceeds $150,000) through withholding or estimated payments to avoid underpayment penalties.

Common Withholding Mistakes

| Mistake | Impact | Solution |

|---|---|---|

| Claiming “exempt” without qualifying | No tax withheld; large bill due | Only claim exempt if you meet IRS criteria |

| Not updating W-4 after marriage or childbirth | Under-withholding | Submit a new W-4 within 10 days of life changes |

| Multiple jobs not accounted for | Combined income pushes you into higher bracket | Use the Multiple Jobs Worksheet on Form W-4 |

| Ignoring state withholding rules | Owe state taxes even if federal is covered | Check state-specific forms and requirements |

Strategies to Avoid Owing Taxes Next Year

Preventing a tax bill starts long before filing season. It requires ongoing awareness and small adjustments throughout the year. Here’s how to take control:

1. Review and Adjust Your W-4 Annually

Even if your job hasn’t changed, your tax situation might have. Did you get married? Have a child? Start a side business? Each of these affects your tax bracket and deductions. Revisit Form W-4 every spring or after major life events to ensure accurate withholding.

2. Make Estimated Tax Payments (If Applicable)

If you earn income without withholding—such as freelance work, rental income, or investment gains—you’re responsible for paying taxes quarterly. The due dates are typically April 15, June 15, September 15, and January 15 of the following year.

Use Form 1040-ES to calculate your estimated payments. Paying consistently helps you avoid both a large April bill and potential penalties.

3. Increase Federal Withholding Strategically

If adjusting your W-4 isn’t enough, consider increasing withholding by a fixed dollar amount per paycheck. This gives you precise control over how much extra goes toward your tax liability each month.

For example, adding $75 per paycheck (on a biweekly schedule) results in $1,950 withheld annually—often enough to cover a typical underpayment gap.

4. Maximize Tax-Advantaged Accounts

Contributions to retirement accounts like a traditional IRA or 401(k) reduce your taxable income. Even mid-year contributions can lower your tax bill. For 2024, you can contribute up to $23,000 to a 401(k) ($30,500 if 50 or older) and $7,000 to a traditional IRA.

Health Savings Accounts (HSAs) also offer triple tax benefits: contributions are deductible, growth is tax-free, and withdrawals for medical expenses are untaxed.

Real-Life Example: How Sarah Avoided a Repeat Tax Bill

Sarah, a graphic designer in Colorado, owed $4,200 in taxes last April. She worked full-time but also earned $18,000 from freelance projects. Because she didn’t make estimated payments and only claimed single status on her W-4, her total tax liability far exceeded her withheld amount.

After consulting a tax advisor, she took three steps:

- Filed Form 1040-ES and began making quarterly payments on her freelance income.

- Updated her W-4 to reflect her combined income and added an extra $100 in federal withholding per paycheck.

- Contributed $6,000 to a traditional IRA, reducing her taxable income and qualifying her for a deduction.

By the next tax season, Sarah broke even—neither owing nor receiving a refund. More importantly, she avoided penalties and gained confidence in managing her tax obligations.

Action Checklist: Steps to Take Now

✅ Prevent Next Year’s Tax Bill – Do This Today:

- Run a tax projection using your current income and deductions.

- Use the IRS Tax Withholding Estimator to check your W-4 accuracy.

- If self-employed, schedule quarterly estimated payments for the current year.

- Consider increasing federal withholding via your payroll system.

- Maximize retirement contributions before year-end.

- Keep detailed records of all non-wage income and related expenses.

Frequently Asked Questions

Can I still adjust my withholding this year?

Yes. Submit a new Form W-4 to your employer at any time. Changes typically take effect within one to three pay periods. While it won’t change your current tax year entirely, it can reduce what you owe next April.

What happens if I owe taxes but can’t pay the full amount?

The IRS offers payment plans, including short-term (up to 120 days) and long-term installment agreements. You’ll still owe interest and possibly a setup fee, but you’ll avoid more serious collection actions. Apply online via IRS Direct Pay.

Is it better to owe or get a refund?

From a financial standpoint, breaking even is ideal. Large refunds mean you gave the government an interest-free loan. Owing a small amount isn’t inherently bad—if planned for. The goal is accuracy, not extremes.

Take Control of Your Tax Future

Owning up to a tax bill is uncomfortable, but it’s also a powerful opportunity to improve your financial habits. Tax planning shouldn’t be an annual scramble—it should be part of your ongoing money management strategy. Whether you’re an employee, freelancer, or retiree, small, consistent actions can keep you in alignment with your tax obligations.

Start today. Review your withholding, track your income sources, and plan for next year’s payments. A few minutes now could save you hundreds—or thousands—down the road.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?