Closing a current account may seem like a simple administrative task, but doing it incorrectly can lead to unexpected fees, damaged credit, or lingering liabilities. Whether you're switching banks, consolidating accounts, or no longer need the service, following a structured process ensures a clean break. This guide walks you through each phase—from preparation to final confirmation—with practical steps, expert insights, and real-world examples to help you close your account without stress or risk.

1. Evaluate Your Reasons and Alternatives

Before initiating closure, assess why you want to close the account. Common reasons include high maintenance fees, poor customer service, better offers elsewhere, or redundancy due to multiple accounts. However, closing an account isn’t always the best move. For instance, if your primary concern is cost, many banks offer fee waivers for maintaining minimum balances or setting up direct deposits.

Consider speaking with a relationship manager. They may offer incentives to retain your business, such as reduced fees, higher interest rates on linked savings, or bundled services.

2. Transfer Funds and Redirect Payments

Ensure all funds are moved out of the account before closure. More importantly, redirect any automatic transactions that rely on this account. Overlooked payments are the most common cause of post-closure issues.

Key Actions:

- Transfer remaining balance to your new or preferred account.

- Update direct debits (utilities, subscriptions, insurance).

- Inform employers or government agencies if this was your salary or benefits account.

- Cancel standing orders and recurring transfers.

Allow at least two full billing cycles after updating payment details to confirm all transactions have settled correctly. Attempting to close too early could result in failed payments and penalties.

“Always allow a grace period after changing direct debits. One missed payment can trigger late fees and affect your credit score.” — Marcus Reed, Financial Advisor at ClearPath Wealth

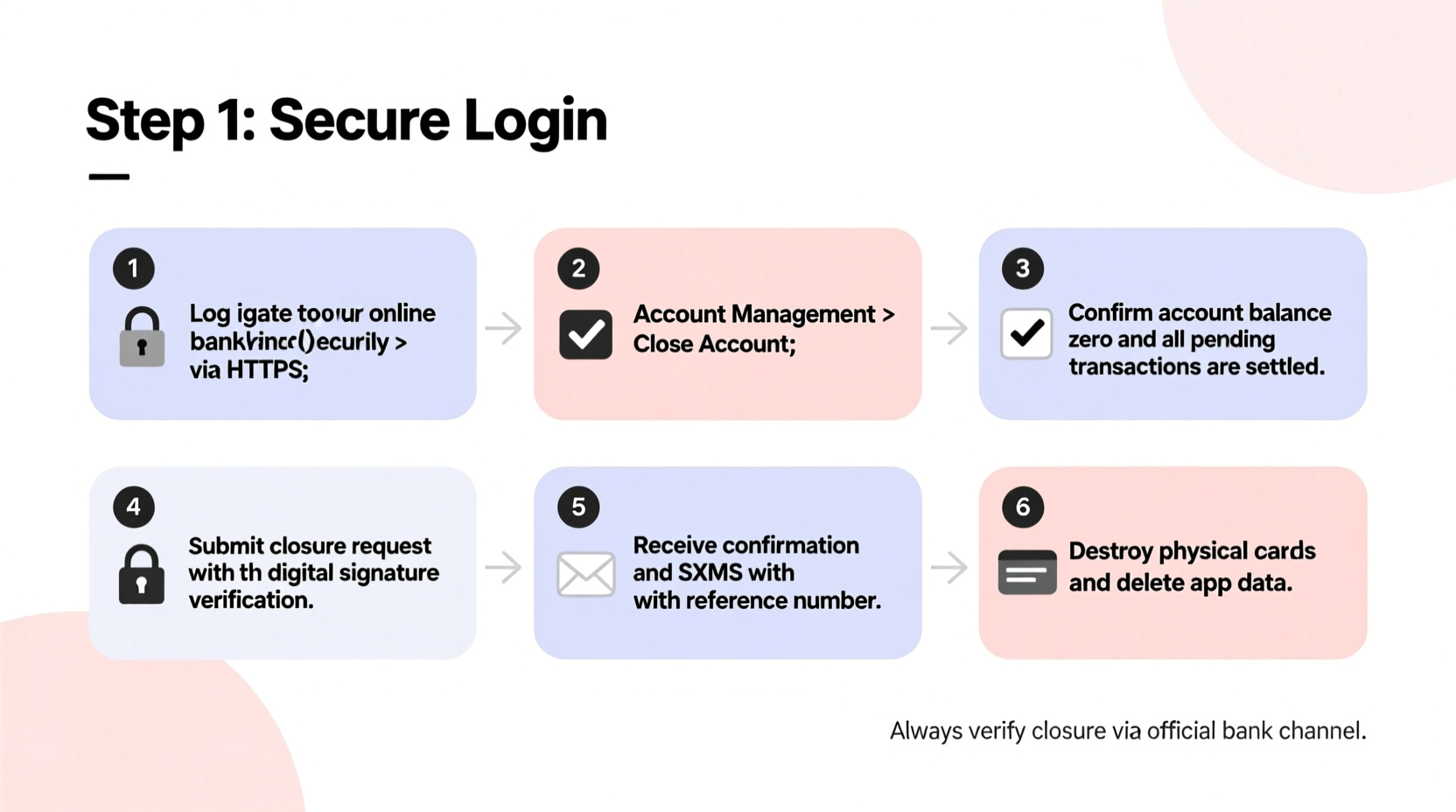

3. Step-by-Step Closure Process

Follow this timeline to close your account systematically:

- Week 1: Review all recent statements and list active direct debits, standing orders, and incoming payments.

- Week 2: Initiate transfers to your new account. Begin updating payment methods with service providers.

- Week 3: Contact your bank via secure channels (branch visit, phone call, or secure messaging) to request account closure.

- Week 4: Confirm zero balance, receive written closure confirmation, and destroy associated cheques and debit cards.

Never assume the account is closed just because you’ve stopped using it. Banks require formal requests, often in writing or authenticated digitally.

4. Official Closure: What to Expect from Your Bank

When you contact your bank, they’ll typically:

- Verify your identity using security questions or two-factor authentication.

- Confirm there are no pending transactions or overdrafts.

- Request return of unused cheques and withdrawal slips.

- Issue a formal closure letter or email confirmation.

If your account has a negative balance, you must settle the amount before closure. Some banks may refuse closure until debts are cleared. In cases of disputed charges, resolve them before proceeding.

5. Security and Post-Closure Best Practices

Closing an account doesn’t automatically erase your financial footprint. Protect yourself from future risks:

- Destroy old cards: Cut through the chip and magnetic strip. Don’t just discard them whole.

- Monitor credit reports: Check your report 6–8 weeks after closure to confirm the account status is listed as “closed by customer.”

- Retain records: Keep bank statements for at least six years in case of audits or disputes.

- Watch for fraud: Monitor for unauthorized activity even after closure—some fraud attempts occur months later.

| Action | Timing | Purpose |

|---|---|---|

| Update direct debits | 2–4 weeks before closure | Prevent failed payments |

| Clear outstanding balance | Before closure request | Avoid rejection or fees |

| Obtain closure confirmation | Immediately after closure | Legal proof of closure |

| Check credit report | 6–8 weeks after closure | Verify accurate reporting |

Mini Case Study: Avoiding a Costly Oversight

Sophie, a freelance designer, decided to close her old current account after opening a new one with cashback rewards. She transferred her balance and canceled her gym’s direct debit. However, she forgot about a monthly cloud storage subscription billed under an old email alias. Two weeks after closure, the payment failed, triggering a $25 late fee and temporary suspension of her files.

After resolving the issue, Sophie realized she should have used her bank’s transaction history from the past 13 months to catch infrequent charges. She now maintains a personal log of all recurring payments and reviews it quarterly.

This example underscores the importance of thoroughness. Infrequent or forgotten subscriptions are among the top reasons for post-closure complications.

Do’s and Don’ts When Closing a Current Account

| Do’s | Don’ts |

|---|---|

| Review 12–13 months of transaction history | Close the account without checking for pending transactions |

| Get closure confirmation in writing | Assume verbal approval means the account is closed |

| Destroy debit cards securely | Throw away cards intact |

| Wait for final statement | Walk away immediately after submitting the request |

Frequently Asked Questions

Can I close my current account online?

Many banks allow account closure through online banking or mobile apps, especially if the balance is zero and there are no active products linked. However, some institutions still require a phone call or branch visit for verification. Check your bank’s policy first.

Will closing my current account affect my credit score?

Simply closing a current account does not directly impact your credit score. However, if the closure results in unpaid bills, bounced payments, or unresolved overdrafts, those negative entries can harm your credit history. Always settle obligations first.

What happens if I forget a direct debit?

If a direct debit fails after closure, the recipient may charge a late fee, and your bank might impose a penalty for insufficient funds—even though the account is closed. Some providers attempt retries over several days. Update all payments proactively to avoid this.

Final Checklist Before You Close

- ✔️ Zero Balance:

- All funds transferred out; no pending deposits or withdrawals.

- ✔️ All Direct Debits Updated:

- Confirmed with service providers; verified successful transactions in new account.

- ✔️ Salary or Benefits Redirected:

- Employer or agency notified with new account details.

- ✔️ Formal Closure Request Submitted:

- Completed via approved channel (online, phone, branch).

- ✔️ Confirmation Received:

- In writing or secure message, stating account is closed.

- ✔️ Cards and Cheques Destroyed:

- Cut up or shredded to prevent misuse.

Take Control of Your Financial Transition

Closing a current account is more than just cutting ties—it's about ensuring every thread is properly managed. By preparing thoroughly, communicating clearly with your bank, and verifying each step, you protect your finances and peace of mind. Whether you're upgrading to a better banking experience or simplifying your financial life, a smooth closure sets the foundation for smarter money management ahead.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?