When setting up a brokerage account, most people focus on investment choices, risk tolerance, and long-term goals. Yet one of the most critical steps—naming a beneficiary—is often overlooked or postponed. Failing to designate a beneficiary can lead to legal complications, prolonged probate processes, and unintended consequences for loved ones. Understanding how beneficiary designations work and why they matter is essential for anyone who wants to protect their assets and ensure a smooth transfer of wealth.

What Happens Without a Beneficiary?

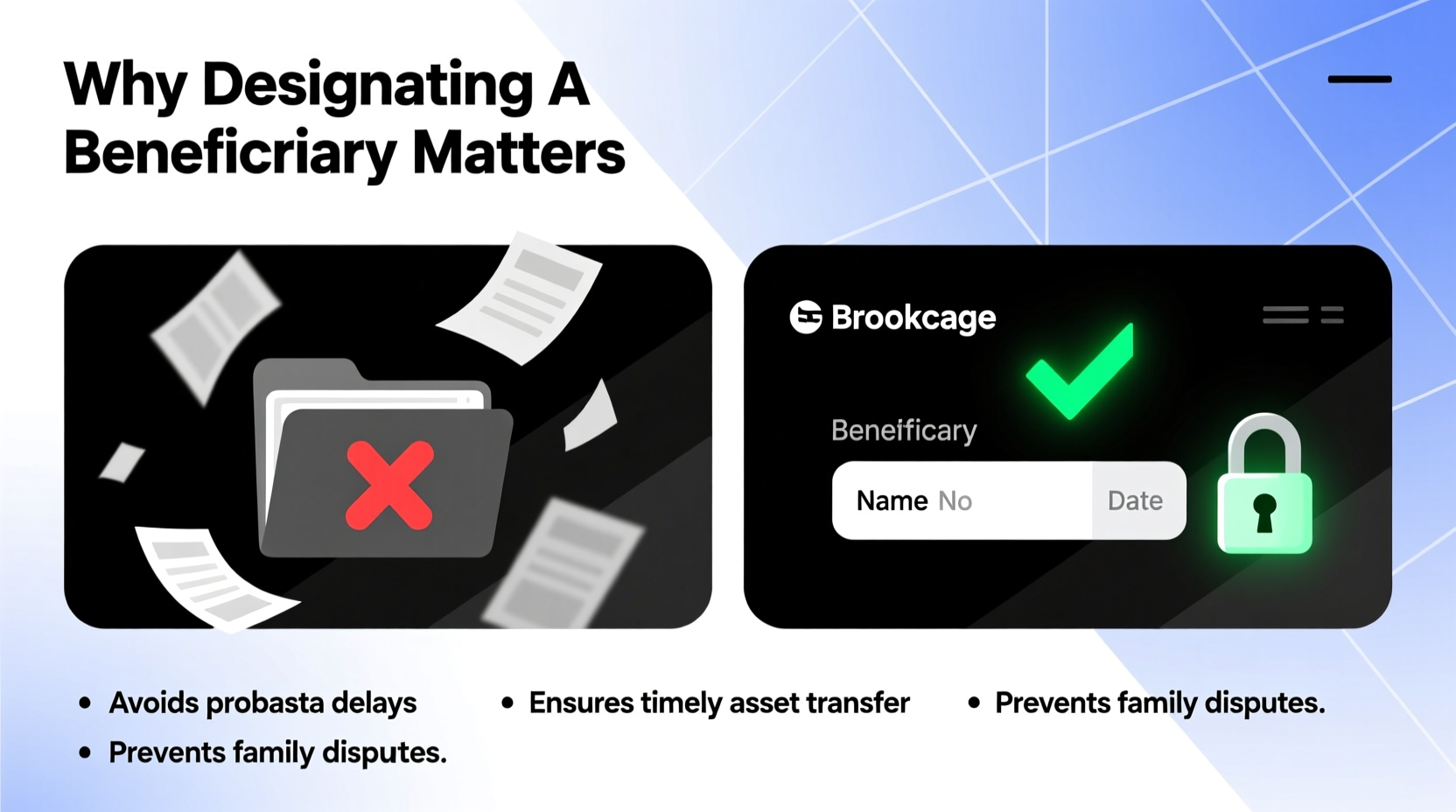

If you pass away without naming a beneficiary on your brokerage account, the assets do not automatically transfer to your spouse, children, or heirs—even if you have a will. Instead, the account becomes part of your estate and must go through probate. This legal process can take months or even years, during which time the funds are frozen and inaccessible to your family.

Probate is not only time-consuming but also public. Your financial affairs become part of the public record, exposing sensitive information about your investments and net worth. Additionally, probate fees, attorney costs, and court expenses can erode the value of the estate, reducing what ultimately reaches your heirs.

“Many people assume their will overrides all asset transfers, but beneficiary designations typically bypass the will entirely. That’s why getting this right is so crucial.” — Laura Simmons, Estate Planning Attorney

How Beneficiary Designations Work

A beneficiary designation is a simple form provided by your brokerage firm that allows you to name one or more individuals, trusts, or organizations to inherit the account upon your death. The transfer happens outside of your will and operates independently of it. This means that even if your will states that assets should go to a different person, the brokerage account will follow the beneficiary form.

You can name primary beneficiaries (who receive the assets first) and contingent beneficiaries (who inherit if the primary beneficiaries predecease you). Most brokerages allow multiple beneficiaries with specified percentages. For example, you might allocate 50% to your spouse and 25% each to two children.

The process is straightforward: log in to your brokerage account, navigate to the “Account Settings” or “Estate Planning” section, complete the beneficiary form, and submit it. Some firms require notarization, while others accept electronic signatures.

Key Benefits of Naming a Beneficiary

- Immediate Access: Beneficiaries can claim assets quickly, often within weeks.

- Privacy: Transfers occur privately, without court involvement.

- Cost Savings: Avoids probate fees and legal expenses.

- Tax Efficiency: Inherited assets may receive a step-up in cost basis, reducing capital gains taxes.

- Control: You decide exactly who inherits and in what proportions.

Common Mistakes to Avoid

Even when people do designate beneficiaries, errors can undermine their intentions. These mistakes are surprisingly common and easily preventable.

| Mistake | Why It’s Problematic | How to Fix It |

|---|---|---|

| Forgetting to update after life changes | An ex-spouse may still be listed as beneficiary | Review and update after marriage, divorce, birth, or death |

| Naming minors directly | Minors cannot legally own large assets; court-appointed guardianship may be needed | Use a trust or custodial account instead |

| Leaving fields blank | Triggers probate and uncertainty | Always name both primary and contingent beneficiaries |

| Duplicate designations across accounts | Inconsistent allocations can cause confusion | Keep records updated and review all accounts together |

Real-Life Example: The Cost of Neglect

Consider the case of Robert, a 67-year-old investor with $420,000 in a brokerage account. He had a will leaving everything to his two children equally but never named a beneficiary on his brokerage account. When he passed away suddenly, the account went into probate. His children spent over $18,000 in legal fees and waited nearly ten months to access the funds. During that time, one child faced financial hardship and couldn’t cover medical bills, despite being entitled to half the inheritance.

Had Robert simply filled out a beneficiary form, his children would have received the assets directly, avoided court costs, and accessed the money within weeks. This real-world scenario underscores how a small administrative step can have massive implications for families during difficult times.

Step-by-Step Guide to Naming a Beneficiary

Designating a beneficiary doesn’t require an attorney or complex paperwork. Follow these steps to secure your legacy:

- Gather your brokerage account information. Know the institution, account number, and login details.

- Determine your beneficiaries. Decide who should inherit the account and in what percentages.

- Log in to your brokerage account. Navigate to the estate planning or account settings section.

- Complete the beneficiary form. Enter names, relationships, Social Security numbers, and allocation percentages.

- Add contingent beneficiaries. Name backups in case your primary beneficiaries die before you.

- Submit and confirm. Print a copy and keep it with your important documents.

- Review annually. Update after major life events like marriage, divorce, births, or deaths.

When a Trust Should Be the Beneficiary

For larger estates or complex family situations, naming a revocable living trust as the beneficiary may be preferable. This approach offers greater control over how and when assets are distributed. For instance, you can specify that a child receives funds in installments or upon reaching certain milestones.

Trusts also protect assets from creditors, divorce settlements, and poor financial decisions by beneficiaries. However, setting up a trust requires legal assistance and ongoing maintenance. Consult an estate planning professional to determine whether a trust aligns with your goals.

Frequently Asked Questions

Can I name my estate as the beneficiary?

Yes, but doing so defeats the purpose of avoiding probate. If your estate is the beneficiary, the assets will still go through the court process, delaying distribution and increasing costs.

What happens if my beneficiary dies before me?

If no contingent beneficiary is named, the assets may revert to your estate and enter probate. Always designate backup beneficiaries to prevent this outcome.

Do retirement accounts and brokerage accounts work the same way?

They operate similarly in terms of beneficiary designations, but tax rules differ. IRAs and 401(k)s have required minimum distributions and specific inheritance rules under the SECURE Act. Brokerage accounts offer more flexibility and often receive a step-up in basis.

Final Checklist: Secure Your Legacy Today

- ✅ Review all brokerage accounts

- Ensure every account has a current beneficiary designation.

- ✅ Name primary and contingent beneficiaries

- Include full names, relationships, and allocation percentages.

- ✅ Avoid naming minors directly

- Use a custodial account (UTMA/UGMA) or trust instead.

- ✅ Update after major life events

- Marriage, divorce, birth, adoption, or death in the family.

- ✅ Coordinate with your overall estate plan

- Make sure beneficiary designations align with your will and trust.

Take Action Now—Your Family Will Thank You Later

Designating a beneficiary on your brokerage account is one of the simplest yet most impactful financial decisions you can make. It ensures your hard-earned investments pass smoothly to the people you care about, without unnecessary delays, expenses, or legal hurdles. Life is unpredictable, and waiting “until later” risks leaving your family vulnerable during a time of grief.

Set aside 20 minutes this week to log in to your brokerage accounts and complete the beneficiary forms. It’s a small effort that delivers lasting peace of mind. Protect your legacy—not just for yourself, but for those who depend on you.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?