In early 2024, NVIDIA (NVDA) was the undisputed leader in the AI-driven market surge, with its stock climbing over 200% in a single year. However, by mid-year, investors began to notice a sharp reversal. Shares that once seemed unstoppable pulled back significantly—prompting widespread concern. So, why is NVIDIA stock down? The answer isn’t singular but rooted in a convergence of macroeconomic pressures, valuation concerns, competitive shifts, and investor sentiment recalibration.

This article breaks down the key reasons behind the recent NVDA dip, evaluates whether the sell-off is justified, and offers insights for investors navigating this volatile phase.

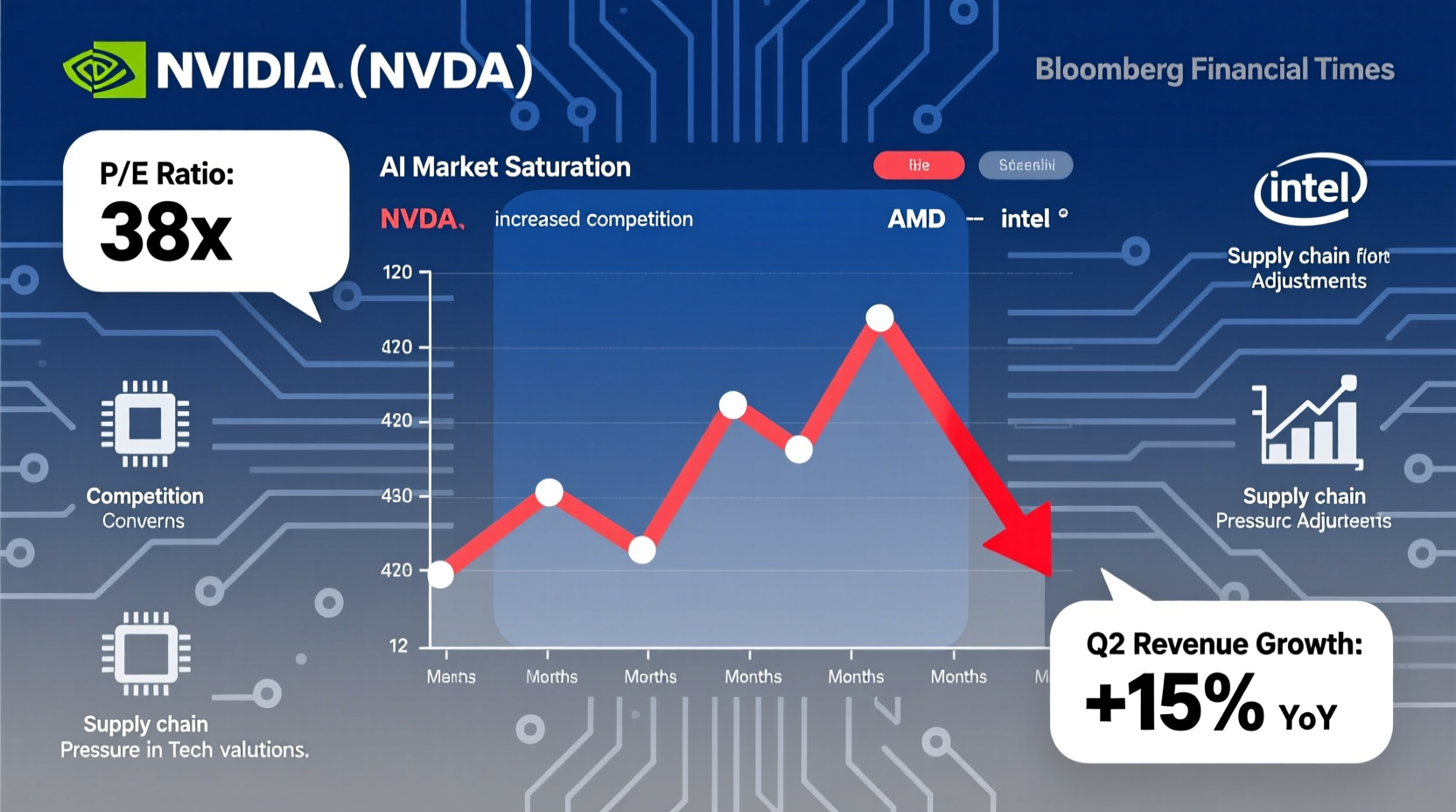

Market Sentiment Shift: From Euphoria to Caution

After a meteoric rise fueled by artificial intelligence hype, NVIDIA reached a peak market capitalization exceeding $3 trillion in June 2024. At that point, its price-to-earnings (P/E) ratio soared above 70—a level historically associated with speculative froth rather than sustainable growth.

As excitement around AI chips reached fever pitch, analysts and institutional investors began questioning whether future earnings could justify such lofty valuations. When broader markets showed signs of weakness—driven by persistent inflation and delayed Federal Reserve rate cuts—high-growth tech stocks like NVDA became prime targets for profit-taking.

“Valuation matters. Even the best companies can see corrections when expectations outpace reality.” — Michael Block, Chief Strategist at Rhino Trading Partners.

The shift wasn’t isolated to NVIDIA. Other AI-related stocks, including Super Micro Computer and Broadcom, also experienced pullbacks. But given NVIDIA’s outsized influence on the Nasdaq Composite, its decline had an amplified effect on overall market psychology.

Supply Chain and Production Concerns

NVIDIA relies heavily on TSMC for the production of its cutting-edge GPUs, particularly the H100 and upcoming B100 models used in data centers. In Q2 2024, TSMC signaled potential delays in its 2nm fabrication process, which is critical for next-gen AI chips.

While not a direct operational failure by NVIDIA, any bottleneck in semiconductor manufacturing raises red flags for investors expecting uninterrupted supply to meet booming demand. Cloud providers like Microsoft, Amazon, and Google have placed massive orders for AI infrastructure, and even minor delays could impact revenue timelines.

Competition Heats Up in the AI Chip Race

For years, NVIDIA enjoyed near-monopoly status in the AI accelerator market, thanks to its CUDA ecosystem and superior performance. But competitors are closing the gap.

- AMD launched its MI300X GPU, showing competitive performance in large language model training.

- Intel continues to push its Gaudi accelerators, offering lower-cost alternatives for enterprise clients.

- Amazon Web Services now uses its custom Trainium and Inferentia chips across internal workloads, reducing reliance on NVIDIA hardware.

- Google has expanded deployment of its TPU v5 chips, further fragmenting demand.

While none of these challengers match NVIDIA’s full-stack advantage yet, their progress signals growing long-term risk. Enterprise buyers are increasingly negotiating better pricing or demanding multi-vendor strategies to avoid lock-in.

Competitive Landscape: AI Accelerator Market Share (Q2 2024)

| Company | Product | Market Share | Key Customers |

|---|---|---|---|

| NVIDIA | H100, A100 | 80% | Microsoft, Meta, Oracle |

| AMD | MI300X | 10% | Microsoft Azure, CoreWeave |

| Amazon | Trainium | 6% | Internal AWS, Anthropic |

| TPU v5 | 3% | Internal, Vertex AI | |

| Others | - | 1% | Specialty vendors |

Though NVIDIA still dominates, the erosion of exclusivity impacts pricing power—a crucial factor in maintaining margins and growth forecasts.

Macro Factors: Interest Rates and Tech Rotation

The Federal Reserve maintained higher interest rates through mid-2024 to combat sticky inflation. This environment penalizes high-growth, high-multiple stocks because future cash flows are discounted more heavily.

NVIDIA, as a forward-looking growth stock, is particularly sensitive to changes in real yields. When the 10-year Treasury yield rose above 4.5%, many fund managers rotated capital into value sectors like energy, financials, and industrials.

Additionally, some hedge funds reduced exposure after realizing substantial gains. According to Bloomberg data, short interest in NVDA increased by 18% between May and July 2024—the highest level in two years—indicating rising bearish sentiment.

What Investors Should Watch Next

A stock correction doesn’t necessarily mean long-term weakness. For those holding or considering NVIDIA shares, here are five key indicators to monitor:

- Earnings Guidance (Q3 2024): Will management reaffirm strong demand from cloud providers and enterprises?

- Data Center Revenue Growth: Slowing YoY growth below 100% may signal saturation.

- New Product Rollouts: Successful launch of Blackwell architecture (B100) is critical for maintaining leadership.

- Geopolitical Risks: Export restrictions on advanced chips to China could limit a significant revenue stream.

- Cash Flow and Buybacks: Strong free cash flow supports shareholder returns and confidence during downturns.

Mini Case Study: The 2022 Crypto Crash Parallel

In late 2022, NVIDIA stock fell nearly 50% from its highs as cryptocurrency mining demand collapsed and gaming sales declined. At the time, many questioned whether the company could pivot successfully to data centers.

Leadership responded by doubling down on AI infrastructure, optimizing chip design for machine learning, and expanding partnerships with hyperscalers. By 2023, data center revenue surpassed gaming as the primary income driver, and the stock rebounded sharply.

Today’s situation echoes that period—not in cause, but in opportunity. While AI demand remains robust, the market is reassessing sustainability. Those who held through the 2022 downturn were rewarded handsomely. A similar patience may be required now.

FAQ

Is NVIDIA stock still a buy after the dip?

Many analysts believe so. As of July 2024, over 80% of Wall Street firms maintain a “Buy” or “Strong Buy” rating on NVDA. The long-term thesis—driven by AI adoption across industries—remains intact. However, timing matters. Dollar-cost averaging can reduce risk in volatile conditions.

How much of NVIDIA’s revenue depends on AI?

Over 70% of NVIDIA’s total revenue now comes from data center sales, primarily AI-focused GPUs. Just five years ago, gaming was the largest segment. This shift underscores both the opportunity and concentration risk in its current business model.

Could another crypto boom help NVIDIA recover faster?

Possibly, but it’s unlikely to be a major driver. Cryptocurrency mining accounted for a brief spike in GPU demand during 2017–2018. Today’s mining hardware is specialized (ASIC-based), and NVIDIA has actively discouraged GPU use in mining with software locks. Future growth will come from enterprise AI, not retail speculation.

Conclusion: Navigating Volatility with Clarity

The recent dip in NVIDIA stock reflects a necessary market correction after extraordinary gains. It’s not a sign of broken fundamentals, but rather a recalibration of expectations. High valuations, competitive threats, supply chain nuances, and macro headwinds combined to trigger a pullback—but the core engine of growth remains powerful.

AI adoption is accelerating, not slowing. Data centers worldwide are being rebuilt around accelerated computing. NVIDIA continues to lead in performance, software integration, and ecosystem strength. Short-term volatility should not overshadow long-term transformation.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?