Mental health care is essential, yet for many, accessing therapy feels out of reach—not because of stigma or awareness, but because of cost. A single session with a licensed therapist can range from $75 to over $200, leaving people wondering: why is therapy so expensive? And if insurance is supposed to help, why does it often fall short? The reality is complex, involving systemic issues in health care financing, provider shortages, and inconsistent insurance policies. But there are solutions—like sliding scale fees—that can make therapy more affordable. This article breaks down the financial landscape of therapy, explores how insurance coverage works (and where it fails), and highlights practical ways to access care without breaking the bank.

The Hidden Costs Behind Therapy Sessions

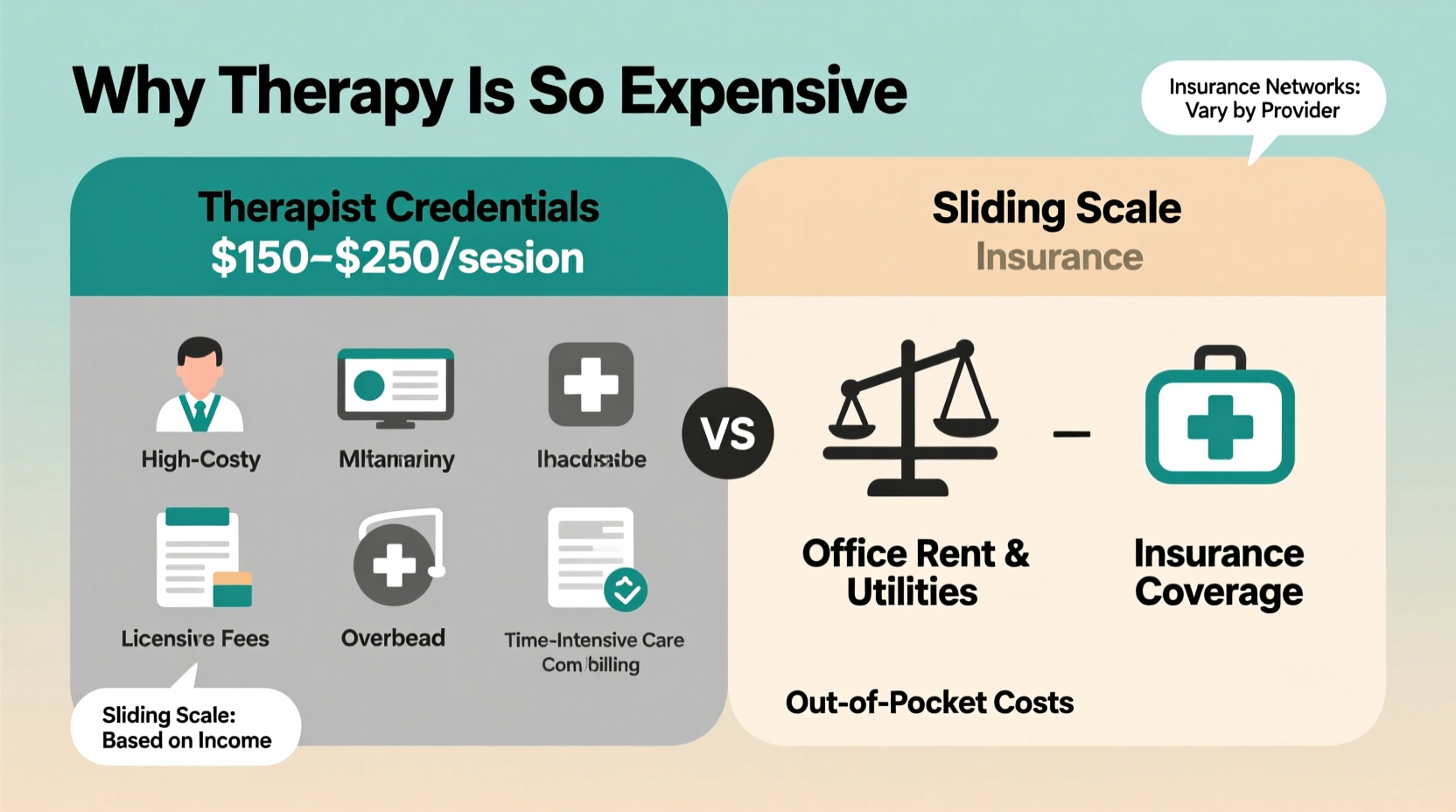

At first glance, an hourly rate of $150 for talk therapy may seem high compared to other services. But unlike a haircut or car repair, therapy requires years of education, clinical training, and ongoing professional development. Licensed therapists typically hold master’s or doctoral degrees, complete thousands of supervised clinical hours, and maintain licensure through continuing education and fees. These requirements ensure quality care but also contribute to higher service costs.

Therapists also face significant overhead. Independent practitioners pay for office space, malpractice insurance, electronic health record systems, billing software, and administrative support. Even telehealth sessions require secure platforms compliant with HIPAA regulations. When you factor in that many therapists work part-time due to emotional burnout or client load limits, their income must cover both personal and professional expenses across fewer billable hours.

Additionally, the supply of mental health professionals hasn’t kept pace with rising demand. According to the Health Resources and Services Administration (HRSA), over 120 million Americans live in areas with a shortage of mental health providers. In such markets, therapists can command higher rates due to limited competition. Geographic disparities further widen the gap—urban centers may have more providers, while rural communities struggle to attract and retain clinicians.

“Therapy isn't just conversation—it's skilled intervention grounded in science, ethics, and deep listening. The price reflects training, responsibility, and time.” — Dr. Lena Torres, Clinical Psychologist and Educator

How Insurance Coverage Works—and Why It Often Falls Short

Many assume that having health insurance automatically makes therapy affordable. In practice, coverage varies widely by plan, provider network, diagnosis, and even state regulations. While the Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008 mandates that insurers cover mental health on par with physical health, enforcement remains inconsistent.

Here’s how insurance typically functions in therapy:

- In-Network vs. Out-of-Network Providers: In-network therapists have negotiated rates with insurance companies, often accepting $80–$120 per session. Patients pay a copay (e.g., $20–$50). Out-of-network providers charge full rate; insurers may reimburse a portion, but patients cover the rest.

- Prior Authorization: Some plans require approval before covering certain types of therapy or extended treatment, delaying care.

- Session Limits: Certain policies cap the number of covered sessions per year, forcing clients to switch providers or pay out-of-pocket after reaching the limit.

- Diagnosis Requirements: To bill insurance, therapists must assign a diagnosable mental health condition (e.g., generalized anxiety disorder), which some clients may not want documented in their medical records.

Even when therapy is technically “covered,” deductibles can be prohibitively high. A person with a $3,000 deductible won’t receive any reimbursement until they’ve spent that amount on health care—including primary care visits, prescriptions, and emergency services. For many, this means paying full price for months before insurance kicks in.

Sliding Scale Fees: Making Therapy Accessible

One of the most effective tools for reducing financial barriers is the sliding scale fee model. Under this system, therapists adjust their rates based on a client’s income, household size, and financial obligations. Someone earning $30,000 annually might pay $40 per session, while another earning $120,000 pays $120—all within the same practice.

Sliding scales are not charity; they reflect a commitment to equitable access. However, availability is limited. Many private practitioners cannot afford to offer deep discounts consistently due to operational costs. Others reserve sliding scale spots for a small number of clients, leading to waitlists.

Despite limitations, sliding scales exist in various settings:

- Community Mental Health Clinics: Federally funded or nonprofit clinics often operate entirely on sliding scales.

- Training Clinics: Universities with psychology or counseling programs run low-cost clinics staffed by graduate students under licensed supervision.

- Private Practices: Some independent therapists allocate one or two weekly slots for reduced-fee clients.

To find sliding scale options, search directories like Open Path Collective, which connects clients with therapists offering sessions for $40–$70, regardless of insurance status.

Real-World Example: Navigating Cost Barriers

Consider Maria, a 29-year-old graphic designer in Austin, Texas. After being laid off during a company restructuring, she began experiencing panic attacks and insomnia. She wanted therapy but faced several hurdles: her new job had a high-deductible health plan ($2,500), and most in-network therapists had 3-month waitlists.

Maria started calling local practices, asking two key questions: “Do you offer sliding scale fees?” and “Are you accepting new clients?” She found a bilingual Latina therapist at a community wellness center who offered sessions for $50 based on income verification. Though not covered by insurance, the cost was manageable. After six months, once her deductible was met, she transitioned to an in-network provider for continued care.

Maria’s story illustrates that affordability often requires research, flexibility, and persistence—but solutions do exist.

Comparison Table: Therapy Payment Options

| Payment Method | Average Cost Per Session | Pros | Cons |

|---|---|---|---|

| Private Pay (Full Rate) | $100–$200+ | Wider choice of therapists; no insurance paperwork; privacy | High upfront cost; not feasible for most without savings |

| In-Network Insurance | $20–$50 copay | Low out-of-pocket cost; structured coverage | Limited provider options; potential session caps; need for diagnosis |

| Out-of-Network Insurance | $75–$150 after reimbursement | Access to specialists outside network | High initial cost; complex claims process; partial reimbursement only |

| Sliding Scale | $20–$80 | Income-based pricing; increased accessibility | Limited availability; may require documentation; waitlists |

| Community/Nonprofit Clinics | $0–$40 | Most affordable; often include additional support services | May lack specialty care; longer intake processes; geographic limitations |

Actionable Checklist: How to Afford Therapy

If cost is holding you back from seeking help, use this checklist to explore realistic pathways forward:

- Review your insurance policy details—call customer service to confirm mental health benefits.

- Search Psychology Today’s therapist directory using filters for “sliding scale” and “insurance accepted.”

- Contact local universities with counseling programs to inquire about low-cost training clinics.

- Reach out to community health centers or nonprofits focused on mental wellness.

- Ask potential therapists directly: “Do you offer a sliding scale or reduced-rate options?”

- Consider short-term or solution-focused therapy models, which may require fewer sessions.

- Explore digital therapy platforms like Open Path or Modest Needs for verified low-cost providers.

Frequently Asked Questions

Does Medicaid cover therapy?

Yes, Medicaid covers mental health services in all 50 states, including individual and group therapy. Coverage specifics vary by state, but copays are typically minimal or nonexistent. Eligibility depends on income and household size.

Can I use an HSA or FSA to pay for therapy?

Yes, both Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) can be used to pay for qualified mental health services, including copays, coinsurance, and sometimes full fees—even for out-of-network providers. Keep receipts for documentation.

Are there free therapy options available?

Truly free long-term therapy is rare, but some options exist: crisis hotlines (e.g., 988 Suicide & Crisis Lifeline), peer support groups (e.g., NAMI), university training clinics, and nonprofit organizations offering pro bono services during mental health awareness months. These can provide temporary relief or supplemental support.

Taking the Next Step Toward Affordable Care

Therapy shouldn’t be a luxury reserved for those with high incomes or perfect insurance. The current system has flaws—uneven coverage, high overhead, and structural inequities—but individuals still have agency. By understanding how insurance works, actively seeking sliding scale opportunities, and advocating for their needs, people can access meaningful care without financial ruin.

Change starts with a phone call, an email, or a simple question: “What options do you offer for clients with limited income?” More therapists are willing to accommodate than you might think. As public demand for mental health services grows, so too does the push for reform—from expanded telehealth parity to state-funded counseling programs. Until the system evolves, informed consumers hold the power to navigate it effectively.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?