Choosing the right business structure can significantly impact your tax obligations, liability protection, and long-term growth. For many small business owners, becoming an S corporation offers an attractive balance of pass-through taxation and limited liability. Unlike traditional C corporations, S corps avoid double taxation because profits and losses flow directly to shareholders’ personal tax returns. However, transitioning to an S corp isn’t automatic—it requires careful planning, eligibility verification, and formal filings. This guide walks you through each essential step to make the election correctly and legally.

Understanding the S Corporation: Benefits and Limitations

An S corporation is not a separate business entity like an LLC or a C corporation. Instead, it’s a tax election made under Subchapter S of the Internal Revenue Code. Once approved, the IRS treats your business as a pass-through entity, meaning income is taxed only at the shareholder level, avoiding corporate income tax.

Key benefits include:

- Tax efficiency: Shareholders can reduce self-employment taxes by splitting income into salary and distributions.

- Liability protection: Owners are generally not personally liable for business debts.

- Credibility: Operating as a corporation may enhance trust with lenders, investors, and clients.

- Perpetual existence: The business continues even if ownership changes.

However, there are important limitations:

- Limited to 100 shareholders (all must be U.S. citizens or residents).

- Only one class of stock allowed.

- Shareholders must be individuals, certain trusts, or estates—not other corporations or partnerships.

- Some businesses, such as financial institutions or insurance companies, are ineligible.

“S corporations offer strategic tax advantages, but they require strict compliance. One misstep in payroll or filing can jeopardize your status.” — Laura Simmons, CPA and Small Business Tax Advisor

Step-by-Step Process to Become an S Corporation

Becoming an S corporation involves both state-level formation and federal tax election. Follow these steps in order to ensure full compliance.

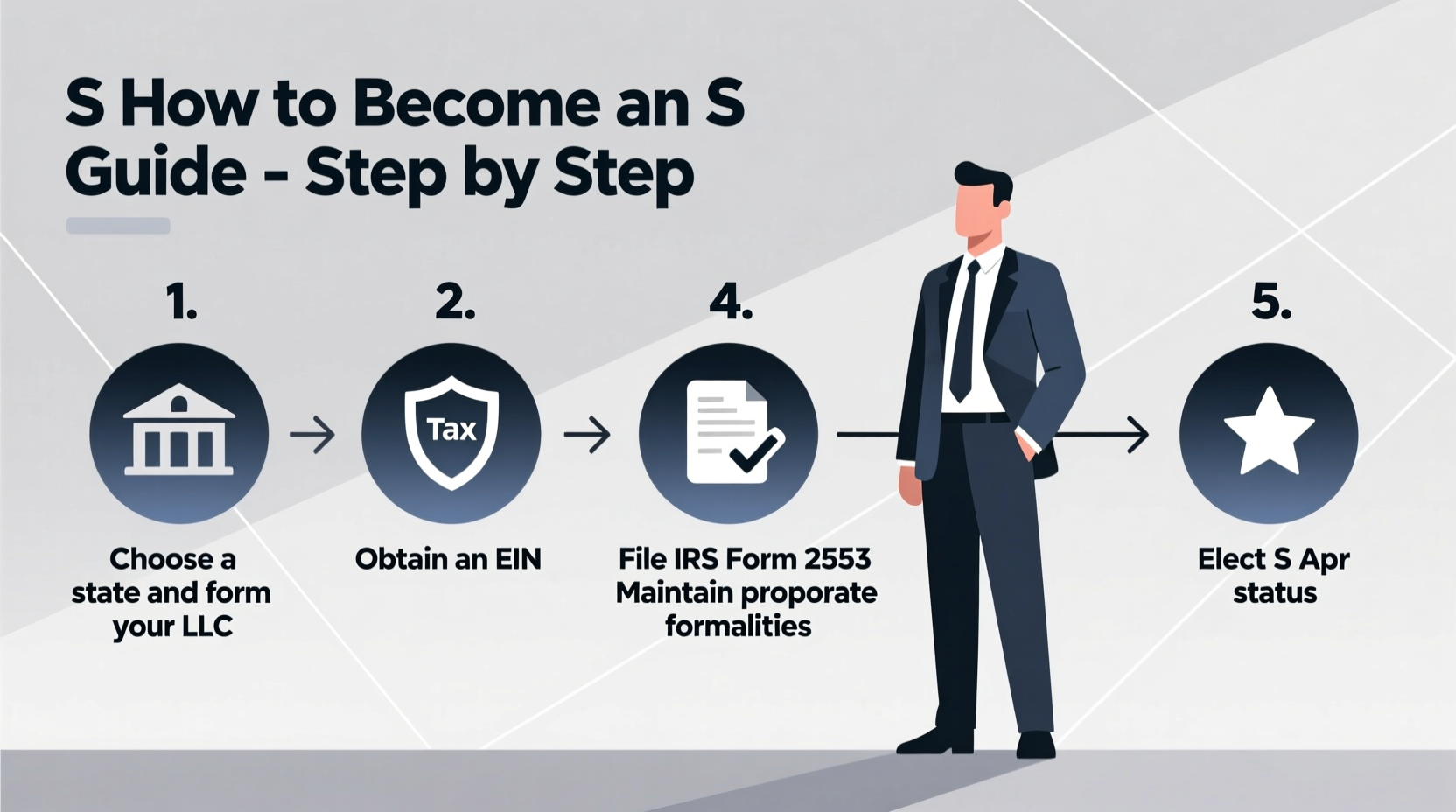

- Form a Qualified Entity

You must first establish a legal business entity eligible for S corp status—typically a domestic corporation or a limited liability company (LLC). Most entrepreneurs incorporate by filing Articles of Incorporation with their state’s Secretary of State office. If you’re converting an existing LLC, you’ll need to check your state’s rules on entity conversion. - Obtain an Employer Identification Number (EIN)

Apply for an EIN through the IRS website. This number is required for tax reporting, opening a business bank account, and hiring employees. Even if you're a sole proprietor, forming a corporation requires a new EIN. - Draft Corporate Bylaws (for Corporations) or Operating Agreement (for LLCs)

While not filed with the state, these internal documents outline governance structure, shareholder rights, meeting procedures, and profit distribution. They help maintain corporate formalities, which is crucial for preserving liability protection. - Issue Stock to Shareholders

Hold an initial board meeting to authorize and issue shares. Each shareholder must receive documentation of ownership. Maintain a stock ledger to track equity changes over time. - File Form 2553: Election by a Small Business Corporation

This is the critical federal form that officially elects S corp status. It must be signed by all shareholders and submitted to the IRS within 75 days of incorporation—or any time during the preceding tax year for current-year treatment.

Eligibility Checklist Before Filing

Before submitting Form 2553, verify your business meets all IRS requirements. Use this checklist to confirm eligibility:

- ✅ Domestic corporation or eligible LLC

- ✅ No more than 100 shareholders

- ✅ All shareholders are individuals, estates, or certain trusts

- ✅ Shareholders are U.S. citizens or resident aliens

- ✅ Only one class of stock (differences in voting rights are allowed)

- ✅ Not an ineligible corporation (e.g., certain financial institutions)

- ✅ All shareholders consent in writing to the election

Real Example: A Consulting Firm Makes the Switch

Sarah Thompson operated her marketing consultancy as a sole proprietorship for three years, reporting $120,000 in annual net income. She paid 15.3% self-employment tax on the entire amount—over $18,000 per year. After consulting with her accountant, she incorporated in Texas, elected S corp status, and began paying herself a reasonable salary of $70,000. The remaining $50,000 was distributed as dividends, exempt from self-employment tax. Her total tax savings in the first year exceeded $7,500, while maintaining full liability protection.

This example illustrates how proper structuring can yield substantial savings—without increasing complexity when managed correctly.

Common Pitfalls and How to Avoid Them

While S corporations offer advantages, mistakes in administration can lead to penalties or loss of status. Consider the following Do’s and Don’ts:

| Do’s | Don’ts |

|---|---|

| Pay yourself a reasonable salary based on industry standards. | Don’t take all profits as distributions to avoid payroll taxes. |

| Keep accurate corporate minutes and hold annual meetings. | Don’t mix personal and business finances. |

| File Form 1120-S annually, even with no income. | Don’t miss IRS deadlines for tax filings. |

| Maintain updated shareholder records and capital accounts. | Don’t issue multiple classes of stock (e.g., preferred shares). |

Frequently Asked Questions

Can an LLC elect S corporation status?

Yes. An LLC can file Form 2553 to be taxed as an S corporation while retaining its flexible management structure. This hybrid approach is popular among single-member LLCs seeking tax savings without corporate formalities.

What happens if I miss the Form 2553 deadline?

The IRS may accept late elections if you can demonstrate “reasonable cause.” Attach a statement explaining the delay and ensure all shareholders sign the form. Alternatively, you can request relief under Revenue Procedure 2013-30 for inadvertent failures.

Do S corporations pay state taxes?

Treatment varies by state. Most states recognize S corp status and do not impose corporate income tax. However, some—including California and New York—levy franchise or minimum fees. Always check your state’s Department of Revenue guidelines.

Final Steps and Ongoing Compliance

After the IRS accepts your Form 2553, you’ll receive confirmation letter (CP261). From that point forward, your business must adhere to S corp requirements:

- File annual Form 1120-S and issue Schedule K-1 to each shareholder.

- Run payroll for owner-employees using a registered payroll service.

- Maintain separate business bank accounts and accounting records.

- Hold shareholder and director meetings with documented minutes.

- Reassess “reasonable compensation” annually based on performance and market data.

Failure to comply with these practices risks IRS reclassification, back taxes, penalties, or revocation of S status.

Take Control of Your Business Structure Today

Becoming an S corporation is one of the most effective ways for small business owners to reduce tax liability while strengthening legal protection. The process demands attention to detail—from entity formation to timely IRS elections—but the long-term benefits often outweigh the upfront effort. Whether you're launching a new venture or restructuring an existing business, taking deliberate steps now can save thousands in taxes and provide greater financial clarity down the road.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?