Whether you're supporting a cause, funding a project, or helping a loved one, how you give can have lasting implications. The terms \"gift\" and \"grant\" are often used interchangeably in casual conversation, but they represent distinct mechanisms of transfer—each with its own rules, expectations, and legal consequences. Understanding the difference isn’t just about semantics; it’s about ensuring your generosity is effective, compliant, and aligned with your intentions.

A misclassified transaction can lead to tax complications, strained relationships, or even legal disputes. This article breaks down the essential distinctions between gifts and grants, explores real-world scenarios, and provides practical guidance for donors, recipients, and organizations navigating the world of financial support.

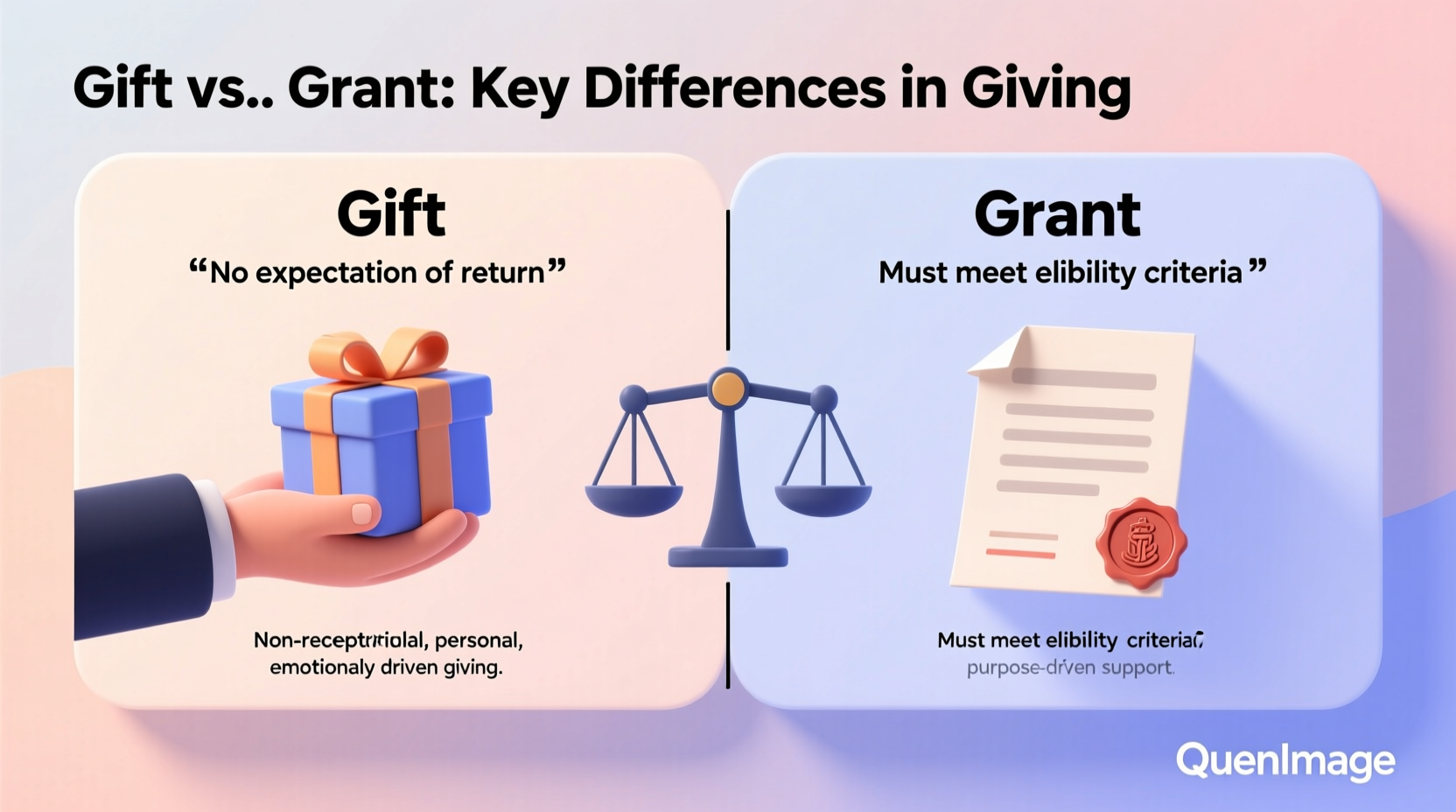

Defining the Terms: What Is a Gift?

A gift is a voluntary transfer of money, property, or assets from one party to another without the expectation of anything in return. Gifts are typically personal, emotional, or familial in nature. They require no formal application, reporting, or performance metrics. Once given, the donor relinquishes control over how the recipient uses the funds.

Common examples include birthday cash from a grandparent, a surprise donation to a friend starting a small business, or a couple funding their child’s wedding. In these cases, there's no obligation for accountability or proof of use. The gesture stands on goodwill and trust.

What Constitutes a Grant?

In contrast, a grant is a structured form of funding awarded based on specific criteria to achieve defined objectives. Grants are almost always conditional. Recipients must apply, meet eligibility requirements, and often report on outcomes. The funder retains oversight and may require audits, progress updates, or repayment if conditions aren't met.

Grants are common in nonprofit work, academic research, government programs, and corporate social responsibility initiatives. For example, a foundation might award a $50,000 grant to a community organization to run a youth mentorship program—but only if the group submits quarterly reports and spends the funds strictly on approved expenses.

“Grants are investments in outcomes, not just goodwill. They require clarity, accountability, and shared goals.” — Dr. Linda Moore, Director of Nonprofit Funding Strategies at CivicEdge Institute

Key Differences Between Gifts and Grants

The line between a gift and a grant may seem subtle, but the implications are significant. Below is a detailed comparison to clarify the distinctions:

| Aspect | Gift | Grant |

|---|---|---|

| Expectation of Return | No expectation of repayment or deliverables | Clear deliverables, reports, or outcomes required |

| Application Process | None; spontaneous or informal | Formal proposal, review, and approval process |

| Accountability | Minimal to none | High; includes financial and impact reporting |

| Tax Implications | May be subject to gift tax if over annual exclusion ($17,000 per recipient in 2023) | Typically tax-deductible for the donor if given to a qualified nonprofit |

| Control Over Funds | Full control transferred to recipient | Funder may restrict usage to specific purposes |

| Duration & Renewal | One-time, unless repeated voluntarily | Often time-bound with potential for renewal based on performance |

Real-World Scenario: When Intent Matters

Consider Maria, who wants to support her nephew’s new bakery. She gives him $10,000. If she calls it a “gift,” he can use the money however he sees fit—even to remodel his kitchen at home. But if she frames it as a “grant” to fund equipment purchases, with the expectation that he’ll provide receipts and a business update in six months, the nature of the transaction changes.

Without documentation, the IRS could later question whether the transfer was truly a gift or an unreported loan or investment. Worse, if other family members feel excluded, the lack of clarity could strain relationships. A simple note stating, “This is an unrestricted gift with no strings attached,” protects everyone involved.

When to Use a Grant Structure

Grants are ideal when:

- You’re funding a specific project with measurable goals

- You want to ensure transparency and responsible use of funds

- You’re a foundation, corporation, or public entity distributing funds systematically

- You seek tax deductions and need proper documentation

Setting up a grant doesn’t require a complex foundation. Even individuals can create mini-grant agreements for causes they care about. For instance, a retiree passionate about literacy might offer a $5,000 annual grant to a local school librarian to purchase books, contingent on a mid-year list of titles acquired.

Actionable Checklist: Choosing the Right Approach

Before making a financial transfer, ask yourself the following questions to determine whether a gift or grant is more appropriate:

- Am I expecting something in return—tangible results, reports, or recognition?

- Do I want control over how the money is spent?

- Is this part of a larger funding strategy or recurring support?

- Could this transaction affect my taxes or estate planning?

- Are multiple parties involved who might interpret this differently?

- Does the recipient need structure and accountability to succeed?

If you answered “yes” to any of the first four, a grant framework may be wiser. If your answers lean toward personal, unconditional support, a gift is likely the better fit.

Step-by-Step: How to Formalize a Grant

Even modest grants benefit from structure. Follow these steps to ensure clarity and effectiveness:

- Define the Purpose: Clearly state the goal (e.g., “Funding after-school art classes for 50 students”).

- Set Eligibility Criteria: Who qualifies? What makes a proposal strong?

- Create an Application: Request a brief proposal outlining budget, timeline, and expected outcomes.

- Review and Award: Evaluate submissions objectively and notify the recipient.

- Draft a Grant Agreement: Include amount, duration, reporting requirements, and permitted uses.

- Disburse Funds: Release payment in installments tied to milestones if appropriate.

- Monitor and Close: Collect final reports and assess impact before considering renewal.

Frequently Asked Questions

Can a gift turn into a grant after it’s given?

No. Once a transfer is made as an unconditional gift, you cannot retroactively impose grant-like conditions. To maintain flexibility, document expectations in writing before transferring funds.

Are grants always larger than gifts?

Not necessarily. The size of the transfer doesn’t determine whether it’s a gift or grant. A $500 grant with reporting requirements is still a grant. Conversely, a $100,000 wedding gift with no strings attached remains a gift.

Do I need to report gifts or grants to the IRS?

Donors must file Form 709 if lifetime gifts exceed the federal exclusion limit ($17,000 per recipient in 2023). Grants to qualified 501(c)(3) organizations are generally tax-deductible and should be documented, but don’t count toward gift tax limits.

Final Thoughts: Clarity Strengthens Generosity

Whether you're writing a check for a family member’s education or funding a community initiative, how you give shapes the outcome. A gift nurtures trust and freedom. A grant fosters accountability and impact. Neither is superior—it depends on your intention, the context, and the relationship.

By understanding the differences between gifts and grants, you protect your interests, honor the recipient’s autonomy, and ensure your generosity creates the change you hope to see. Thoughtful giving isn’t just about the amount; it’s about the clarity behind it.

浙公网安备

33010002000092号

浙公网安备

33010002000092号 浙B2-20120091-4

浙B2-20120091-4

Comments

No comments yet. Why don't you start the discussion?